0

0

Dear Mom,

You’ve taught me the value of trusting in others and hoping for the best and I’ve been very successful as a result. Now is the time for me to show you how I’ve learned to apply what you taught me.

I’ve learned that people who make money with other people’s money won’t necessarily tell you everything you need to know when it is your money. For example, that mutual fund representative who told you that now was a good time to invest in the stock market didn’t tell you that the market hadn’t reached a historical valuation bottom. When he said that it might go lower, he didn’t mention that it had always gone lower from the market levels on Mother’s Day 2009 after a speculative top like in 2000.

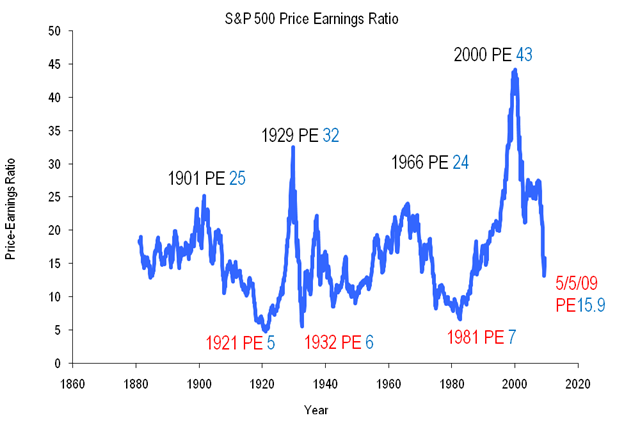

I’ve learned that you should listen to people who don’t get paid if you invest. People like Robert Shiller who wrote Irrational Exuberance explaining the market cycles. Professor Shiller keeps the Price Earnings valuation chart from his book updated on the internet for anyone to look at for free at http://www.irrationale… (this uses 10 year average earnings to smooth out variations.) The chart below shows that the S&P 500 stocks have not hit the historical bottoms like they did after the peaks in 1901, 1929 and 1966. On May 5, the S&P 500 was more than twice as high as the historical bottom so you could lose one half your investments if you invest today.

I’ve learned that the internet has made it easier to find data you can trust. Standard & Poor’s calculates the S&P 500 stock market index and puts the data and future earnings estimates online at www2.standardandpoors….SP500EPSEST.XLS. Currently, the last 12 months reported earnings have a PE of 119. Standard & Poor’s does not project the PE ratios to improve until after the 3rd quarter 2009.

Finally, I’ve learned that our government officials don’t have the courage to control things that are obviously going wrong. When Alan Greenspan was Chairman of the Federal Reserve he had access to the same charts that you do so he could see that the stock market was at historic highs yet he didn’t even try to talk down the market. Now, we have banks that are not lending because they are broke yet our current Treasury Secretary and Federal Reserve Chairman are not taking the actions needed to quickly fix these problems. Maybe their plan will work eventually but history states it will take years, maybe more years than you have left.

A retired widow like you should wait until after the market bottoms to risk any money in the market. In fact, the best Mother’s Day Gift I can give you is to convince you to sell all your stocks after the recent rally.

Your Son,

The One Eyed Guide

S&P500 PE History

In sales, there is a technique to make buyers decide to purchase called the “Ben Franklin Close”. It is a simple two column list with all the reasons to buy on one side and all the reasons not to on the other. The side with the greatest number of reasons shows which decision to make.

A broad stroke look like this of where the market is likely to go is useful if you are a mutual fund investor whose investments generally follow the whole market, or someone who’s willing to invest in inverse funds to benefit from downside moves. My list on whether to buy or sell the current market is shown below:

|

Reasons S&P500 will Go UP (BUY) |

Reasons S&P500 will Go DOWN (SELL) |

|

1. The market is still down 42% from its highs |

1. The market is up 25% from its lows. |

|

2. There is a lot of cash on the sidelines |

2. Market volume is moderate, at best. |

|

3. There are signs of improvement in the economy |

3. The economy decline was worse than anticipated in the first quarter, which could get even worse as initial reports are revised. |

|

4. The government has undertaken unprecedented monetary stimulus. |

4. Corporate earnings are forecast to decline until the 4th quarter (Standard & Poor’s) |

|

5. The government has some fiscal stimulus starting to kick in. |

5. Standard & Poor’s estimates that the S&P 500 will have a negative price/earnings (P/E) ratio in the third quarter of 2009 |

|

6. There has been some improvement in consumer confidence surveys and reported spending |

6. Dividends are declining (S&P500 first-quarter 2009 dividends $5.96, down from $7.15 in fourth quarter 2008) |

|

|

7. P/E ratios never hit the historic bottom. Currently S&P500 is about 15. The high historic bottom is 8 and the recent market bottomed at 12. (Based on 10 year averages as calculated by Robert Shiller) |

|

|

8. Housing prices continue to decline and could reach the levels of 2002 if the Japan experience is duplicated. |

|

|

9. The initial stress test shows that banks are still undercapitalized so lending will continue to be weak. |

If you have more reasons the market will go up, please add them in the comments. There are more reasons to put onto the down side but the list is already too depressing.

If you’re cautious, then the best thing is to be out of the market. If you’re aggressive than there seems to be more downside from here than there is upside and inverse funds are an opportunity for you.

If you’re a stock picker there are plenty of value stocks to pick from today though I’m personally waiting for the next leg down to buy.

I enjoy observing the evolution of the economy, but we should name the new animals that have been created.

Modern bankruptcy laws were implemented in 1898 after literally hundreds of years of experience proved that debtor’s prisons were ineffective. After all, if someone has no money putting them in prison simply eliminated the opportunity for them to make money to repay their debts. Since then, businesses have been trying to eliminate the opportunity for individuals to get out of debt, though they have never come up with a solution to most debtor’s major problem: lack of money.

The 2005 revision to the bankruptcy law tried to make sure people would try to repay debt. One section of it eliminated the opportunity for bankruptcy courts to modify “mortgages on primary residences by placing the portion above the market value of the house on par with other unsecured debts.” The logic in 2005 was that the financial companies that owned the mortgages would be better at judging whether to modify them than a bankruptcy judge. In 2009, we have some reason to doubt the judgment of finance companies.

In any case, I’ve never understood how banks could justify removing bankruptcy protection for primary residences while leaving it for second homes and investment properties. … When enacted, this clearly encouraged individuals to undertake moral hazard by gambling with the bank’s money on vacation homes and investment properties. It actually did this in practice (along with a lot of other distorting factors) as 1/3 of homes sold in 2005 were second or vacation homes. These vacation and second homes represent the majority of excess housing in the United States.

Worse, making primary residences a unique class of assets distorts the system and slows down the “creative destruction” that is key to renewal of an economic system. The questions this note addresses are:

1. “What is the rationale behind continuing this distortion?”

2. “What should this rationale to be called?”

This could simply be a distortion to benefit financial companies which could be called Bankism, the preference of banks and other financial companies over other interests. This is certainly prevalent in today’s government with preference for financial institutions’ interests over those of taxpayers.

However, the recent refusal by the Senate to repeal this distortion may indicate that it is part of a larger trend to favor business (and managers) over the interests of private individuals. The net result of the primary residence exclusion is to favor ownership by business over ownership by individuals. After all, the current rule holds the individual 100% responsible for paying too much for his home and eliminates the ability of the bankruptcy judge to hold the bank at least partly responsible for lending more than the home was worth.

What do you call favoring business ownership over private ownership? If Capitalism is the private ownership of property and Socialism is the state ownership of property, is tilting the rules of ownership of property in favor of business “Business Socialism”, “Business Capitalism” or something new like “Businessism”?

Back to top

Back to top{kind=link}